In last month’s article we spoke through how to measure the real impact of Paid Brand Search campaigns.

The consistent insight we find across brands is that 10% of our attributed conversions from Paid Brand Search campaigns are driven by what we do in Paid Brand Search.

So the natural follow-on question is: what is driving the other 90%?

Let’s get into that one today.

What’s driving the other 90%?

As we went through last week, one of the huge benefits of the nested MMM answer to Brand Search is that we understand what is actually driving brand search volume.

People don’t search for brands by accident.

We know that people don’t wake up in the morning and search for brand names for no reason.

Something must have happened to generate that search behaviour.

Knowing that your brand search demand is increasing is really valuable. It is a great indicator of long term success.

It tells you that you are doing the right things at a macro level.

𝗕𝘂𝘁 𝗸𝗻𝗼𝘄𝗶𝗻𝗴 𝘄𝗵𝗮𝘁 𝗶𝘀 𝗱𝗿𝗶𝘃𝗶𝗻𝗴 𝘁𝗵𝗮𝘁 𝗶𝗻𝗰𝗿𝗲𝗮𝘀𝗶𝗻𝗴 𝗱𝗲𝗺𝗮𝗻𝗱 𝘁𝗲𝗹𝗹𝘀 𝘆𝗼𝘂 𝘄𝗵𝗶𝗰𝗵 𝗼𝗳 𝘁𝗵𝗼𝘀𝗲 𝘁𝗵𝗶𝗻𝗴𝘀 𝘆𝗼𝘂 𝘀𝗵𝗼𝘂𝗹𝗱 𝗱𝗼 𝗺𝗼𝗿𝗲 𝗼𝗳.

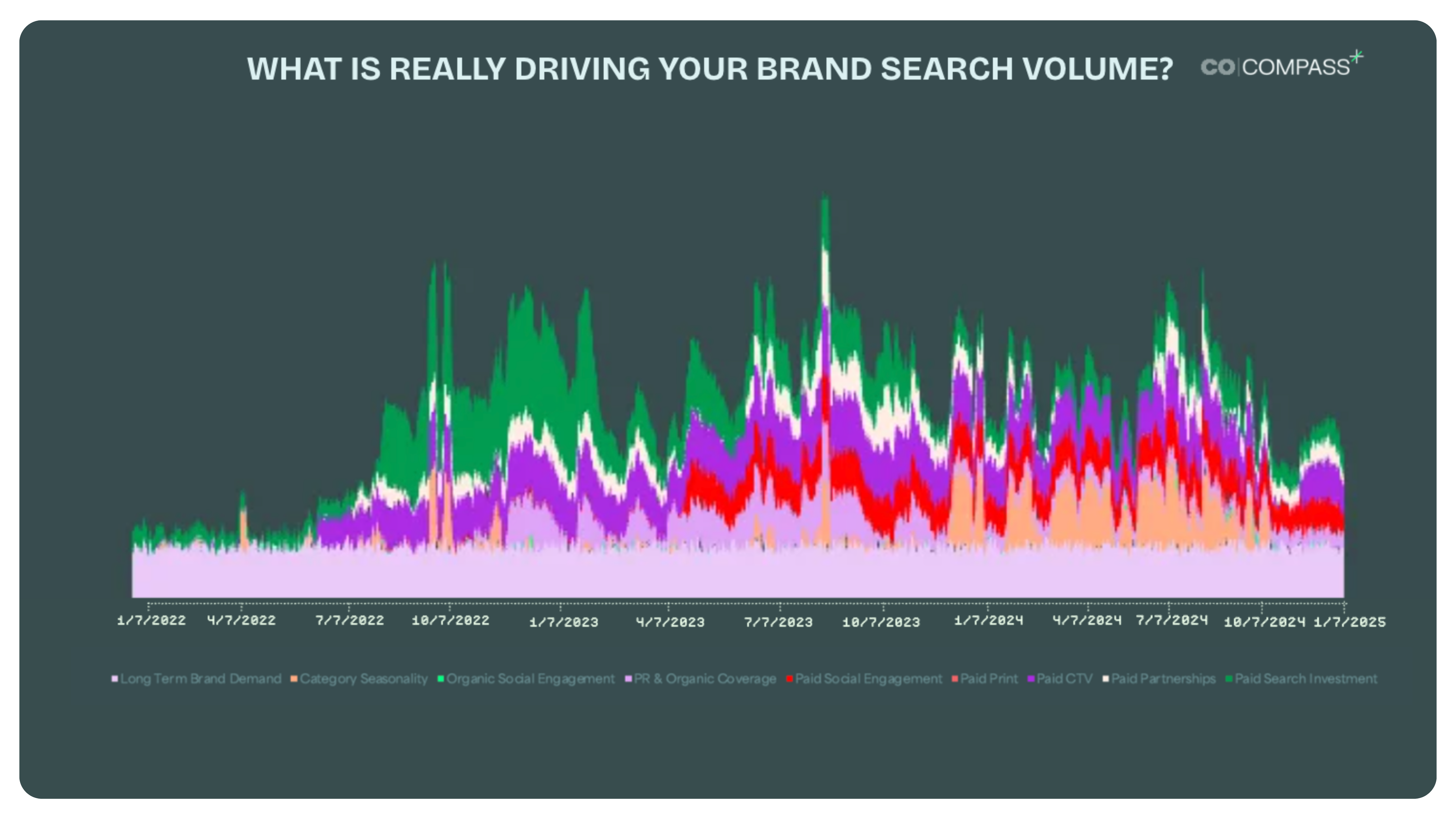

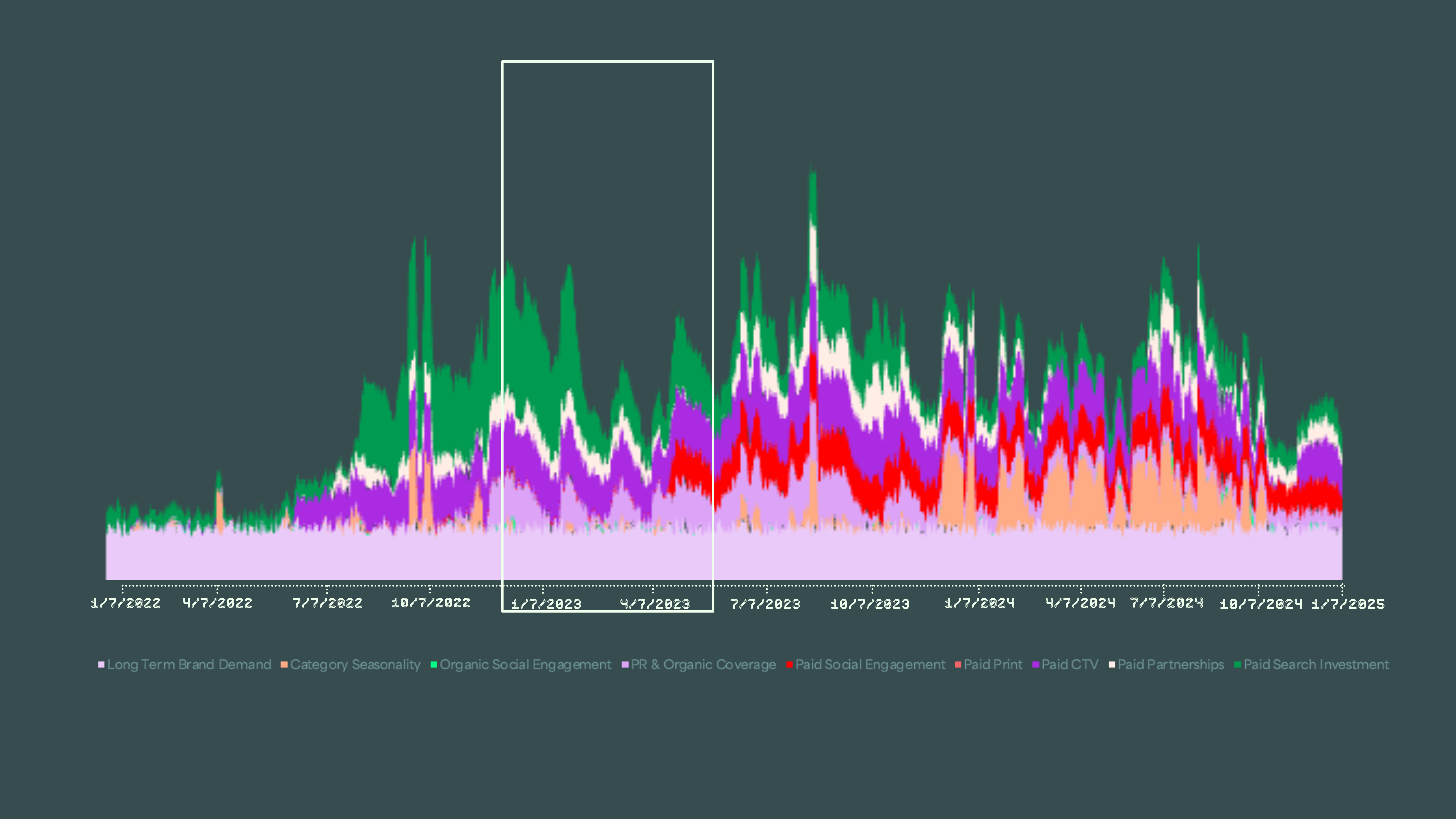

This brand demand is made up of both long term slow changes and short sharp spikes.

You can see on the chart below, there is a long term base which is relatively unreactive to medium term marketing investments. Then there are some category seasonality impacts which create significant spikes, but we have little control over.

𝗕𝘂𝘁 𝘁𝗵𝗲𝗿𝗲 𝗶𝘀 𝗮𝗹𝘀𝗼 𝗮 𝗹𝗼𝘁 𝗼𝗳 𝗶𝗺𝗽𝗮𝗰𝘁 𝗳𝗿𝗼𝗺 𝗯𝗼𝘁𝗵 𝘀𝗵𝗼𝗿𝘁 𝘁𝗲𝗿𝗺 𝗮𝗻𝗱 𝗹𝗼𝗻𝗴𝗲𝗿 𝘁𝗲𝗿𝗺 𝗺𝗮𝗿𝗸𝗲𝘁𝗶𝗻𝗴 𝗶𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁𝘀.

We run models which measure increase in brand search demand, alongside our models which measure increase in revenue.

It helps give a view to the longer term lens alongside shorter term performance.

So what makes up these contributions over time?

Every brand is different, and these behaviours will change for every brand in every market.

But when we compare across multiple brands and categories we see some trends.

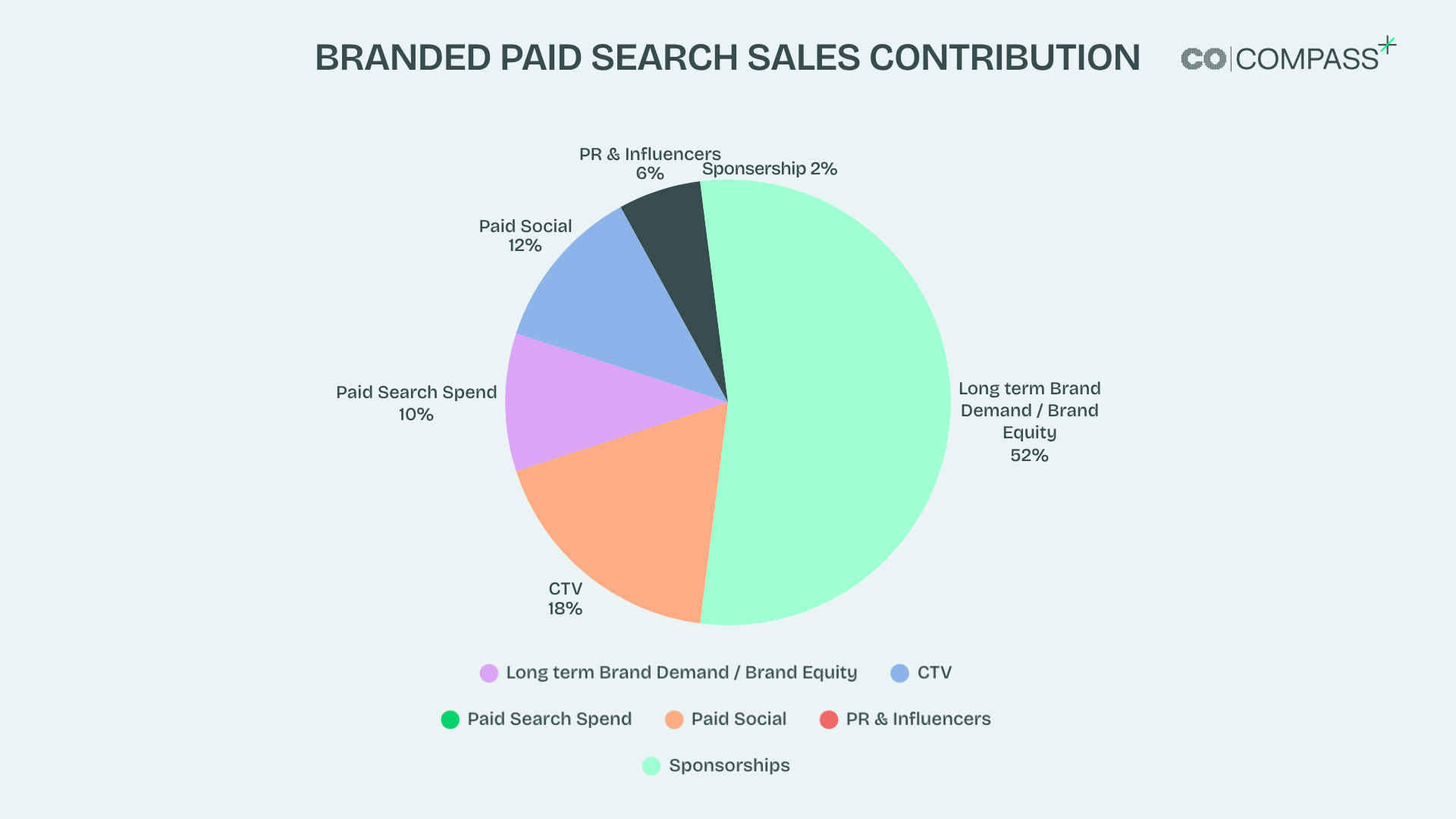

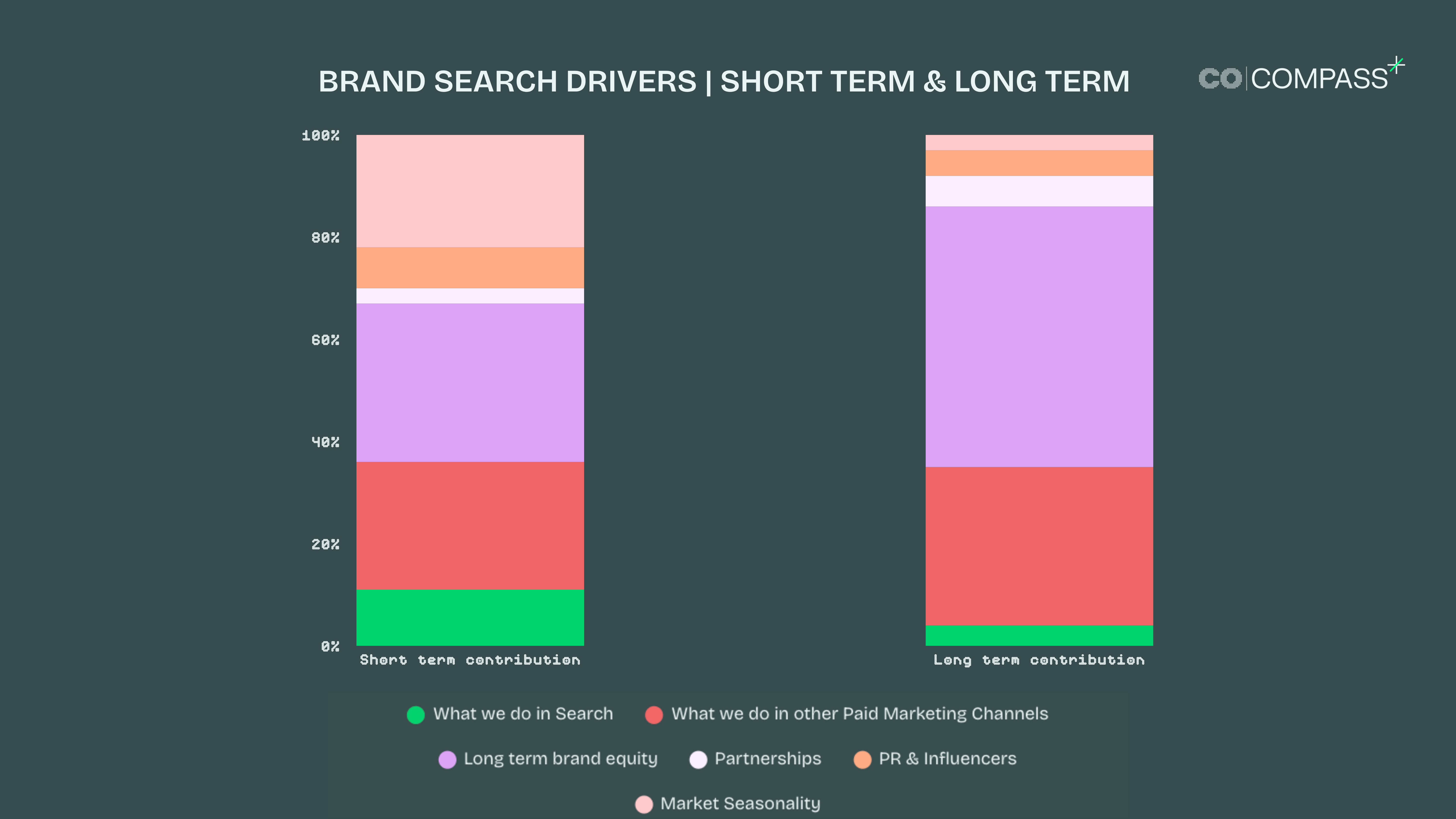

- Around 15% 𝗼𝗳 𝘁𝗵𝗲 𝗯𝗿𝗮𝗻𝗱 𝘀𝗲𝗮𝗿𝗰𝗵 𝗽𝗿𝗲𝘀𝗲𝗻𝗰𝗲 𝗶𝘀 𝗱𝗲𝗽𝗲𝗻𝗱𝗮𝗻𝘁 𝗼𝗻 𝘁𝗵𝗶𝗻𝗴𝘀 𝘄𝗲 𝗱𝗼 𝘄𝗶𝘁𝗵𝗶𝗻 𝗣𝗮𝗶𝗱 𝗦𝗲𝗮𝗿𝗰𝗵. If you increase non brand search presence then some of those people will go on to search for your brand name. This effect tends to be bigger on competitor campaigns, some people in-market for competitors will discover you on competitor campaigns and come back on your brand terms (though the high relative cost of competitor campaigns can still make this a negative ROI impact).

- Category seasonality usually represents around 25% of short term variation, but has virtually no impact on long term trends.

- Around half of brand search volume is driven by long term brand equity. The marketing activities you ran years ago. Most brands could turn off all paid marketing campaigns and keep around half your brand search volume in the short term. This obviously varies significantly based on brand size and duration, a long established brand like Coke Cola would see much higher brand equity impact, a newly launched brand would have virtually none.

The rest of the impact is from what we do in other marketing channels.

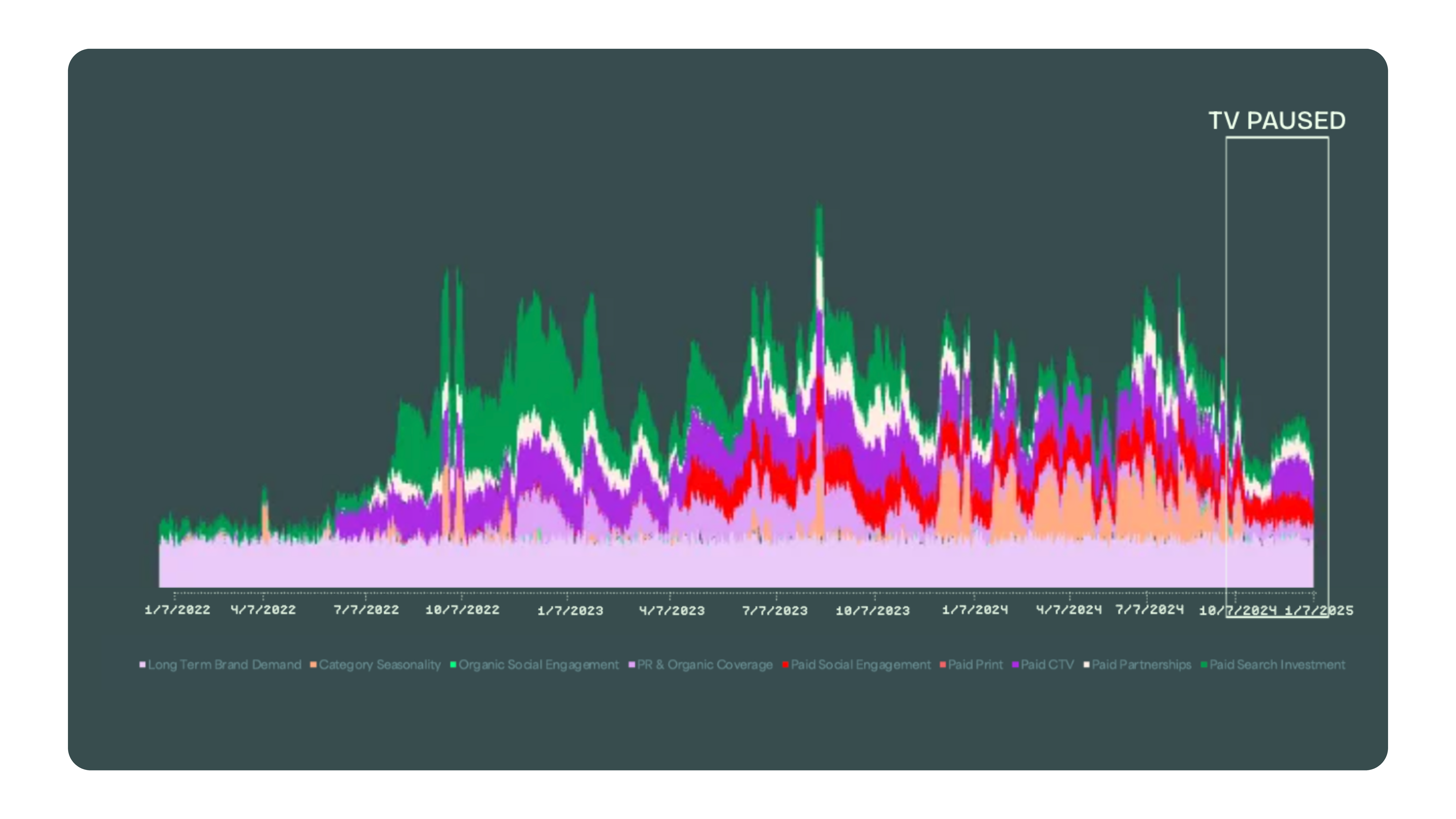

Brand Search is significantly reactive to TV / CTV. Driving both short term spikes and long term sustained growth (spot the dips when this investment is reduced / paused).

Even for ecommerce, digitally native brands, broad reach TV and CTV activity is one of the biggest levers to pull to move this brand search volume.

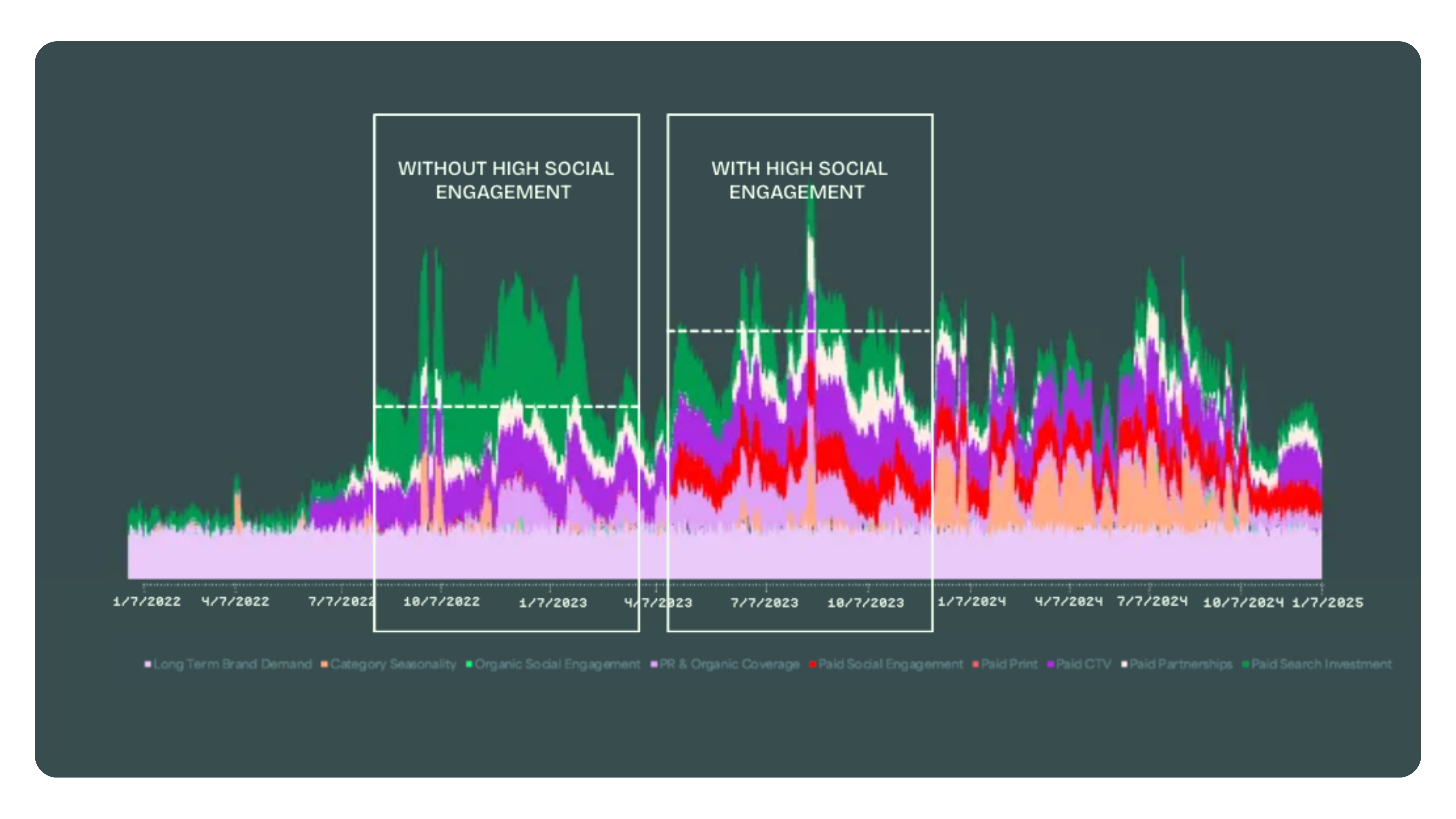

Paid social is a huge driver of search. We can see the really strong contribution from paid social engagement highlighted in red, and can see the significant impact it makes to the underlying volume across the brand before and after ramping up social engagement volume.

Some of the biggest sustained spikes in brand search volume can be attributed back to PR and influencer content. This shouldn’t surprise anyone. 80% of impact from influencer content is indirect (people not clicking on content, but showing up later in search or organic channels). These indirect uplifts are a crucial mid term growth lever for brand search volume.

Partnership activity is some of the hardest to measure, but brand search uplifts give a great short term proxy to show the longer term benefits. Highlighted below in yellow, these partnership activities (in this case, sponsorship of sports teams) drive both sustained long term impact and short term spikes through partnership amplified content. A brilliant mix of short and long term contribution while pushing the brand out to new audiences that would be hard to activate through paid marketing channels.

When we combine all those impacts together, we get 10% of our brand search volume is dependent on what we do in search in the short term, but only 4% in the longer term.

What we do in other paid channels is twice as important in the short term and nearly 8 times more important in the longer term.

Long term brand equity explains around a third of short term spikes and troughs, and more than half the long term trend.

Partnerships and Influencers give us some significant (but smaller) contributions in both the short and longer term.

And seasonality causes a lot of short term spikes but very little impact on the long term.

We know that brand search volume is a crucial measure of future success, but it has a lot of dependencies.

One of the weakest levers is what we do in search, especially in the longer term.

One of the strongest is how we show up in other marketing channels, particularly more broad reach channels such as CTV

We can make significant impacts through partnerships, PR and influencers. Which all tend to be undervalued by short term measurement.